In The News

We’re a regular contributor to MoneySense magazine and the Financial Post. We were invited to the 2018 Federal budget lock-up and were published in Macleans Magazine. In 2016 we entered a National financial planning competition and placed 2nd over-all.

“I just wanted to let you know how much I enjoy your articles in money sense. I read them as they come out and am learning so much from you. Thank you for your well written, concise articles.”

Financial hardship withdrawal exceptions and increasing income in retirement

Money in a LIRA or LIF is intended to last a lifetime, making it difficult to access more than the maximum withdrawal amount. There are a few unlocking exceptions, though.

I am in B.C., Canada. I moved my LIRA into a LIF two years ago. I have taken the maximum annual withdrawals for each year. I thought it’d be smart to start taking it.

How do I know if it’s time to increase the risk in my retirement portfolio?

This 76-year-old man gets $15,000 from his RRIF annually, but is worried he won’t have enough money.

Q: I’m a 76-year-old, single male with $272,000 in a registered retirement income fund (RRIF) and it’s invested in a low-fee exchange-traded fund that is split 50-50 between equities and fixed income.

Using a HELOC as an investment strategy: not as taboo as you might think

Would leveraging the equity in a home to invest in dividend-paying investments lead to tax repercussions?

I wish to leverage my HELOC to invest in dividend-paying investments. How would you advise I approach this? Is this an effective tax savings tool? Is there any financial institution or products you would advise?

How to model retirement income in Canada

The risk of having too much money left when you die is real. Often realizing this comes too late in life. Here’s how to avoid that now.

I am retired early at 58 years old. My wife is 56 years old. We live on a Christmas tree farm, which was paid for years ago. I have a work pension, and my wife was bought out for her pension. We have considerable RRSPs, farm income, and farm property. Where do we start to see how much we can spend a month?

Should I invest more in REITs since I don’t own any real estate?

REITs can be a good addition to an investment portfolio, but they should not be added just because you don’t own a home, experts say.

Q: I plan to rent for most of my life, mainly because I move around the country a lot to advance my career. Would it be prudent to invest more money in real estate investment trusts (REITs) to make up for the fact that I don’t own any real estate?

Where should working retirees put extra income: A TFSA or an RRSP?

Working Canadian retirees may look at CPP and OAS as extra income. Is putting that money in a TFSA or RRSP the better choice?

I will be receiving CPP and OAS as of June 2024. I intend on working one more year until I reach 66. My question is: Should I put all my CPP money into an RRSP to shelter it from tax? Or should I pay the tax on it and invest in a tax-free savings account?

I’m only 31 years old. Do I have to save and invest for retirement?

Take a balanced approach to investing and goal setting so you have a good life now and in the future, experts say.

Q: I’m 31 years old and new to saving and investing. This may sound like a silly question, but do I need to just save for retirement? Almost everything I read or watch about investing is always tied to your retirement funds, but can you invest just to make some extra money to be used in, say, five to 10 years from now? What if I want to throw some money into index funds and let it grow for a few years, then cash out to pay for school, buy a new car or put a down payment on a house?

Does it make sense to make early RRIF withdrawals for my 4 kids to avoid tax?

What is sometimes forgotten with RRSP/RRIFs is the real advantage of the tax-free compounding they provide.

Q: I am a 64-year-old widow with four adult children who are the beneficiaries of my estate. My pension is adequate for my living expenses. I have $620,000 in registered retirement savings plans (RRSPs), which will be taxed at 40 per cent upon my death. I plan to convert a portion of my RRSP to a registered retirement income fund (RRIF) and withdraw $20,000 annually starting in 2024. I would rather pay tax on this additional income every year.

Should seniors cancel their life insurance policies?

At what point do we no longer need life insurance? You will find the answer by going back to the basics and reviewing your current life insurance needs. My husband is about to turn 60 and we have to make a decision to continue with a life insurance plan or to let it go. We no longer have a mortgage, and we are in process of taking care of our own funeral arrangements, so our kids don’t have to worry about it. I’ve been retired for over a year, and he plans to retire at 62.

Q: Do we need life insurance still or should we be OK to let it go?

What’s the difference between a defined benefit and defined contribution pension plan?

Both plans are good, but quite different, and each plan has its own variations.

Q: I know that a lot of workers who change jobs go from defined-benefit (DB) pension plans to defined-contribution (DC) pension plans at their place of work. How can I figure out how much money I’ll really end up with in retirement? And what are the pros and cons of each of these plans?

I want to retire now at 48, but how do I figure out if I can afford to?

After a few ‘what if’ questions, this financial planner was able to come up with a workable solution.

Q: I’m 48 years old and not sure how much longer I can continue working at my job. I don’t enjoy it anymore. What would happen if I stopped working now? I earn $170,000 annually. My 51-year-old husband Tom is self-employed and earns $40,000 annually. Our home is worth $1 million and has a $170,000 mortgage.

CPP and disability: When should you retire and start your pension?

When collecting disability, retiring early is an option. But find out how that can impact disability income and retirement plans.

Q: I have a brain injury and I’m collecting CPP disability of $15,000 a year, along with a workplace disability income of $16,000 a year. I am 61 years old, married, and I can’t figure out if I should retire now and start my pension or wait until I turn 65. My pension projections show that, if I retire now, I will get $29,905 a year, indexed, dropping to $20,034 a year at age 65.

If you knew when you were going to die and the money you would leave, what would you do differently?

The answer is ‘nothing’ if you are doing proper financial planning.

Q: If you knew both your date of death and the amount of money you would leave behind, let’s say $1 million, what would you do differently?

Making a plan: How to withdraw money from a retirement account

Canadians have quite a few options for retirement savings. But before you look at when to retire and start withdrawing, create a plan first.

Q: I have a $180,000 DC pension plan from my old employer, and I have to decide whether to transfer it to a LIRA within Manulife as a personal plan (where the group plan is right now), or to transfer to another LIRA (ETF direct investing with my bank). I am 52 and am considering retiring at 55. I have about $120,000 in RRSP. I also have an LAPP of approximately $600 a month, if I start collecting it at age 65.

My three kids chose different educational paths. How do I withdraw RESP funds in a way that’s fair to them and avoids unnecessary taxes?

A Certified Financial Planner explains how RESP withdrawals and taxation can work for each of your children, regardless of their educational path.

Q.I have a registered education savings plan (RESP) for my three children, the youngest of whom is starting university this fall. We have made some withdrawals for the older two kids but the plan is still well-funded. Our middle child has decided to pursue a co-op university program, which is essentially self-funded.

What’s the best way to minimize taxes when gifting two rental properties?

Parents want to give their daughter a townhouse and a condo.

Q: My parents own real estate and would like to give two of their rental properties (a condo and a townhouse) to me. Is there a way of setting up a trust to transfer rental property without tax implications? I read about a common estate-planning strategy where you can do an estate freeze with a discretionary family trust, which locks in the current value of an investment portfolio or a business. I also read there are tax-deferral benefits. Is this true? And what would the benefits be?

What are the ins-and-outs of splitting RRIF income with a spouse to get the $2,000 tax credit?

For most people, it makes sense to convert enough of your RRSP to a RRIF and claim the pension tax credit.

Q: I just turned 65 years of age and still work full time. To take advantage of the $2,000 pension tax credit, I need to convert at least some of my registered retirement savings plan (RRSP) into a registered retirement income fund (RRIF) so that I can withdraw $2,000 each December as qualifying pension income. My question is, if I set this up today, can I withdraw the $2,000 and claim it as qualifying pension income for 2023?

DC plans once you retire: What do you do with them?

When coming up to retirement, should your investments move with you. Find out the options for soon-to-be retirees. registered and unregistered investments, but would you favour one over the other? My oldest sibling is 99 years old, and I have four other siblings in their 90s. My husband, who was an only child, had parents who lived to be 84 and 89, respectively.

Q: My husband has an DC RPP through an insurance company and will retire within the next year. It is his only pension, although we have other non-registered investments. We are anticipating receiving $25,000-plus a year from this pension.

Can we retire in 7 years at 55 even though we have a $525,000 mortgage now?

Couple could retire with $60,000 income a year, but they need to think about the kind of lifestyle they want.

Q: My wife Helen and I are 48 years old. We would like to stop working at age 55. Is this attainable for us? We owe $525,000 on our mortgage and our home is valued at $1.1 million. We currently pay a mortgage of $1,845 biweekly at an interest rate of 2.99 per cent with a 30-year amortization schedule. We hope to pay off the home within seven years and are making extra payments of $30,000 per year. We plan to live in this home and potentially sell it if we cannot live there anymore because of illness or aging.

What’s the best way to use RRSP contribution room accumulated through rental income?

In this case, expert advises forgetting about the RRSP contributions and focusing on the big picture instead.

Q: I am 66 years old, retired and have about $30,000 of net rental income total from two rental properties I inherited when my dad passed away two years ago. I have gross income — including Canada Pension Plan (CPP), Old Age Security (OAS), a small pension as well as the net rental income — of about $95,000 annually. I also have $100,000 in my registered retirement savings plan (RRSP). I understand that net rental income creates RRSP contribution room. What’s the best way to make use of this extra room over the next few years? I plan on leaving an estate to my two children who are now in their 40s.

Registered vs unregistered accounts: Where retirees should make withdrawals

When you have the choice for withdrawals, it makes sense to look at the pros and cons of taking money from registered and unregistered accounts.

Q: We are in the age bracket where we need to take RRIF withdrawals every year. I am 81, and my husband is 82. We also have an unregistered account. We need to withdraw additional money to pay our expenses. We have already taken the mandatory withdrawal for this year from our RRIF. Our TFSAs are fully funded. I know there are pros and cons of making withdrawals from registered and unregistered investments, but would you favour one over the other? My oldest sibling is 99 years old, and I have four other siblings in their 90s. My husband, who was an only child, had parents who lived to be 84 and 89, respectively.

What kind of CPP split can I expect from my former spouse?

Service Canada will work out the CPP credit split based on years living together, pensionable earnings.

Q: I have just received my divorce papers and want to apply for a Canada Pension Plan (CPP) credit split. I had been married for 30 years and I expect my former spouse to contest the CPP split. Should I be worried that he’ll get to keep his entire CPP? He is self-employed and was the main breadwinner throughout our marriage, though I worked some full- and part-time jobs on and off after the children went to school. Any insight you could give on what may happen with the CPP split would be appreciated.

Can I retire at the end of this year given the recent downturn in the markets?

You have enough to retire if you are comfortable with your situation, expert says.

Q: My wife Caroline is 61 years old, retired from her job in southern Ontario last year, and is now doing a little part-time work. I’m 63 and planned to retire from my consulting job at the end of this year, but I’m not sure I can afford to, given the extended downturn in the stock markets. My registered retirement savings plan (RRSP) has $210,000 and my tax-free savings account (TFSA) has $61,000. I also have $180,000 in my corporation, but this will increase to $250,000 by year-end.

How to calculate the taxable amount for a cashed-in whole life insurance policy

Is a whole life insurance cash value taxable? Spoiler: Yes. But find out how to calculate the taxable amount.

Q: I cashed in my whole life insurance policy last year and received a T5 suggesting I have to pay tax on the full amount of my cash value. Is this correct? The cash surrender value was $27,000, I paid $28,000 in premiums, and they told me my pure cost of net insurance was $30,000, whatever that means. It doesn’t make sense to me! When I purchased the policy, I was told I could use this money for my retirement. I don’t remember the insurance agent ever saying anything about tax.

How should I invest my money now if I’m expecting an inheritance in 10 to 20 years?

Single mom has paid off her mortgage and figures she can save $20,000 annually.

Q: I am a single mom with two teenage daughters. I make $90,000 annually and apart from paying my mortgage and having $20,000 in a tax-free savings account (TFSA), I don’t have any investments. But I turned 50 this year and made the last payment on my condo, so I am mortgage free. Going forward, I will be able to save about $20,000 annually and plan to invest that money in a registered retirement savings plan (RRSP) and tax-free savings account (TFSA).

How to have the most tax-efficient retirement income plan

Should you plan your retirement savings around paying the least amount of taxes? Find out the implications and the better solution.

I am 59 years old, semi-retired and live in Ontario. I have $302,000 in my non-registered investment account (mostly Canadian equities), $133,000 in my TFSA (in equities), and $287,000 in my RRSP (in equities). I have three non-registered GICs, in 1-, 2- and 3-year terms, all earning approximately 4.3%. Each contains $25,000. Lastly, I have a savings account with $20,000 earning 4.250%.

I’m 73 and newly widowed so how should I best organize my finances and investments?

Keep in mind the three wealth destroyers as your analyze your new financial situation.

Q: I am 73, newly widowed and struggling with how to set up my investments as well as with how to minimize taxes on a fixed income. I’d love some tips on how to get things organized as well as who to look to for help. Any suggestions?

Should I include a pension as part of my fixed-income holdings when determining my asset mix?

If volatility bothers you, including your pension in your portfolio allocation may not be a good idea.

Q: When calculating your asset mix, should you include a pension as part of your bond/cash holdings in a portfolio with a mix of 60 per cent in equities, 20 per cent in bonds and 20 per cent in cash? If you had a pension that was paying $450,000 a year, this would be equal to a $1-million guaranteed investment certificate (GIC) at four per cent. Am I thinking about asset allocation correctly? Or should I be taking something else into consideration?

Can you maximize your RRSP and TFSA with an income of $0?

With a year of no income, find out if it makes sense to max out registered accounts like an RRSP and a TFSA, and what other options investors may have.

Q: I have $119,000 room allowed in my RRSP and $81,000 room in my TFSA. I am 47, live in B.C., currently not earning income as a caregiver for a parent. I have a business with a registered GST number to claim income now or in the future. But for my question, let’s assume I will be claiming $0 for the next three years. I have a sum of $250,000 coming to me as a gift, and I am looking to invest/save it.

Can we retire on $170,000 in savings and maintain our current lifestyle?

Expert says couple may need to work longer, reduce their lifestyle expenses and more.

Q: Our retirement is fast approaching and we’re not sure what to do. I’m 68, self-employed, incorporated, with a family trust and a holding company of which I am the sole shareholder. In addition to my small Canada Pension Plan (CPP) and Old Age Security (OAS), I’m drawing dividends of $120,000 per year and there’s enough income left annually to dividend $60,000 to my holdco as well as to pay my wife Rita, 59, a salary of $40,000 per year for bookkeeping services.

What are REITs and how do they fit into a balanced portfolio?

Here are a few things to think about before adding a REIT, or any other themed investment.

Q: I’ve read a lot of articles lately recommending investing in real estate investment trusts (REITs). What are they exactly and how do you invest in them? How do I know if they are a good investment for me and how are they taxed? Finally, I have always had a balanced portfolio of 60 per cent equities and 40 per cent fixed income. How would REITs fit into my portfolio mix?

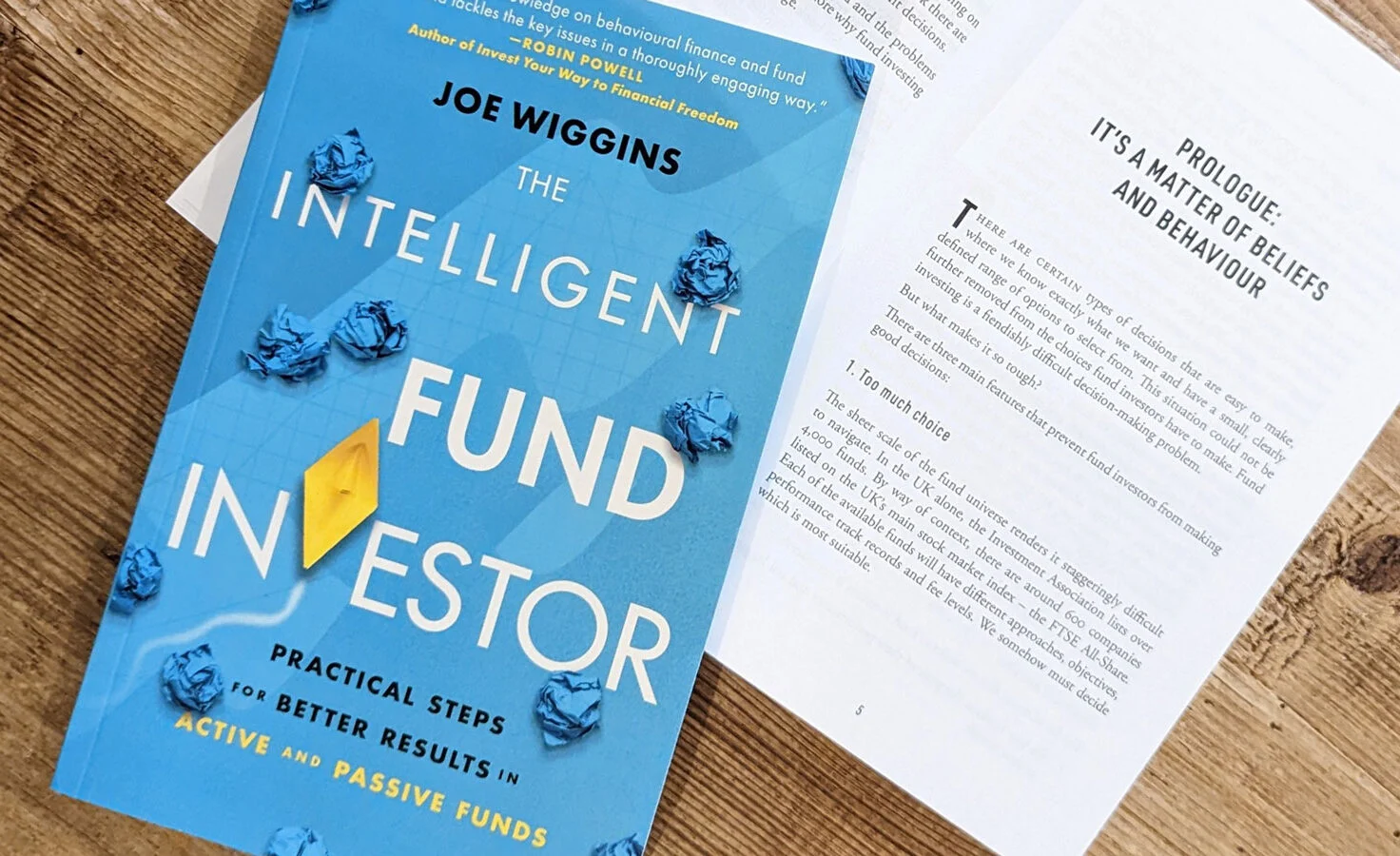

Book review: The Intelligent Fund Investor by Joe Wiggins

Selecting funds based on past returns, stories about “the next best thing” and so on can be costly mistakes. This book explains why, so you can avoid them.

Wow! I just finished Joe Wiggins’ new book, The Intelligent Fund Investor (Harriman House, November 2022). What a great read—I’d recommend it for both DIY and professional investors. There’s no fluff, and I comfortably read through every chapter, right to the end—something I don’t always do.

Is there any advantage to continuing CPP contributions after age 60?

The simple answer is you don’t have a choice.

Q: I am 60 years old and have paid into the Canada Pension Plan (CPP) for the past 38 years, most of them at the maximum. I am now self-employed and working part time, making about $130,000 annually. Is there any advantage to me continuing to pay into the CPP for the next five years until I start drawing CPP?

We’re in our 50s, but do we have enough to retire next year on $70,000 per year?

Here’s what you need to consider while preparing your DIY retirement plan.

Q: I have been the sole income earner while my spouse stayed home to raise our kids. After working for 35 years, I want to retire soon. I’m 56 years old and my wife Mary is 53. My plan is to work through to the end of 2023. I have run my numbers through retirement calculators and while I see the first three years as possibly lean, I am somewhat comfortable with the whole picture. My wife, however, wants me to work longer. She cannot see how we can go from living off $145,000 gross per year down to $70,000 gross.

How to plan for retirement in five or 10 years

When deciding to retire in five or 10 years, there are a few things to consider, in addition to your mortgage, debt and work and government pensions..

I am a divorced empty nester and a registered nurse, who is trying to figure out how to plan the next five to 10 years, before my retirement. Currently I am a 55-year-old female, and I will have a pension from my workplace. Unfortunately due to life circumstances, I did not start my company pension until I was about 40 years old.

Should I commute my pension and take $1.1 million to retire now?

Make sure you’ve taken a good long look at yourself in the mirror before making a move.

Q: I am conflicted on whether I should wait to take a defined-benefit pension in four years at age 60, which would be approximately $80,000, or take a transfer value of $1.1 million and retire now. The market right now scares the crap out of me, so I haven’t done it. What would taking the transfer value look like? I have maximum contribution room in my and my spouse’s registered retirement savings plans (RRSPs).

Should I put my seven rental properties into a corporation? Or is there a better option to save on taxes?

There may be no annual tax savings by adding rentals to a corporation, especially if you are a highly paid employee.

Q: I have seven rental properties in my name. Should I put them into a corporate structure? What is the benefit (if any) of doing this? Are there any better options? Right now, I’m reporting the income and losses on these on my personal tax return.

Tax-efficient retirement strategy options for Canadians

A Canadian couple wonders about winding down their taxable investments. A Certified Financial Planner looks at the options.

Q: My husband and I have a modest portfolio of just under $700,000—no company pension. My husband is 79, and I am 66. We have only taken the minimum out of our RRIFs—my husband’s amount has always been based on my age. Over the past few years we haven’t had to pay taxes, as I am self-employed part-time and work from our home. I have been able to write off a portion of our carrying costs.

Is whole life insurance a good investment? If so, in what circumstances?

If you have a large or complicated estate, it pays to take a look at insurance, experts say.

Q: “My wife and I are both 50 and have two kids. Our household income is about $200,000 a year, evenly split between my wife and I. I’d like to leave a large inheritance to my two kids. Is it ever a good idea to buy a whole life insurance policy as an investment vehicle? Why or why not? And if not, what would be a better option?

The tax implications of gifting adult children money and more

A reader asks about investing in his RRSPs after 71, withdrawing from RRIF and a sizable gift of money to his daughter would affect her tax-wise.

Q: I am a widower, turning 71 before the end of the year. I have annual gross income of about $50,000, cash savings of about $500,000 left from the sale of my principal residence and an RRSP of about $1.5 million returning about 8%. I haven’t put anything into my RRSP for about 15 years. I also have a fully paid vacation property valued at $300,000. I am concerned that I will have to collapse some of my very productive investments to cover the government withdrawal rate of 5.28%.

Best investment strategies for newcomers to Canada

This family has an extra $10,000 they’d like to grow.

Q: I will be immigrating to Canada in November with my spouse and three children, and I need advice on the investment opportunities a new immigrant can take advantage of. We have done a budget of our landing costs and have realized that we have an excess of $10,000 CAD outside the cost of living expenses for six months.

Can I put mutual fund fees back in my account?

Investing fees (MER, TER, trailing) are always hard to swallow, but what if there was a way to manage with mutual funds? Take a read to find out.

Q: I have DIY investments and have recently discovered they are receiving the 1% I was originally paying to my financial advisor. I’m a buy-and-hold mutual funds investor and I was trying to get away from paying the advisor the 1% he would take every year for just giving me a report on the growth.

Is our conservative investment plan really the right one for us?

Knowing your lifestyle wants will lead to appropriate asset allocation decisions, experts say.

Q: I’m 71 and collecting Canada Pension Plan (CPP), Old Age Security (OAS) and Guaranteed Income Supplement (GIS). My husband Dave is 61 and collecting a CPP disability pension that will be replaced by regular CPP at age 65. The payments will then likely only be a very low $1,800 per year. I have $550,000 in a registered retirement savings plan (RRSP) as well as $40,000 in a tax-free savings account (TFSA), while Dave has $70,000 in an RRSP and $40,000 in a TFSA. Together, we own our townhouse in Calgary and are mortgage free.

Why do I need a financial plan?

Before deciding if you need one, know what a financial plan is, the benefits, how it is analyzed and how it can affect you today and in the future.

Q: I am in my early 50s, have a steady job, I’m not a big spender, and I make RRSP contributions. Why would I need a financial plan? I don’t see how it could help me.

What is a pension bridge and should I take it?

Think lifetime lifestyle and insurance to guide your decision.

Q: I’m retiring next year at age 59 and have a defined-benefit (DB) pension plan with my employer, so I will need to make some choices before starting it. What is a pension bridge benefit in a DB plan? Should I take or forego this option? I also need to decide on the percentage of the survivor benefit of my pension that will be payable to my spouse, Richard, upon death. There are several options. Richard doesn’t have an employer pension, but has roughly $250,000 in his registered retirement savings plan (RRSP) and plans to retire later than me — in four years when he reaches age 65. He has worked part time for the past 10 years and earns roughly $40,000 annually. What other options should I pay attention to? I don’t want to make a mistake.

Annuity vs. GIC: What makes sense for retiring?

Can you compare apples to apples with annuities and guaranteed investment certificates for retiring? Let’s find out.

Q: I’m 60 right now. And, if I buy an annuity for $100,000, it appears I can get about $510 per month, according to the best quote I see, which is $6,120 a year. If I take the same $100,000 and get 4.2% interest on it at current rates, I can take out $536 a month for 25 years, which is my life expectancy.

My portfolio is down 30%. Do I still have enough to retire this year?

You might have to employ the three Cs of financial planning: Create, Convert, Conserve.

Q: I’m set to retire later this year and my portfolio is down 30 per cent. What should I be doing? I don’t know if I have enough money to retire anymore.

What happens to CPP and OAS payments when a spouse dies and how do we plan for this?

Lifestyle planning should be the first step in your overall plan so you can have a good life both now and in the future.

Q: My spouse and I are doing some retirement planning and running some projections on future income in retirement. But we’re wondering what happens to Canada Pension Plan (CPP) and Old Age Security (OAS) payments in retirement when a spouse dies? Any info would help.

What’s the best way to maximize my RRIF money?

Contrary to popular opinion, drawing extra to minimize high after-death taxes might not make financial sense.

Q: I’ve always believed it’s best to draw down one’s registered retirement income fund (RRIF) or life income fund (LIF) to zero by about age 85 to 90 to minimize the end-of-life tax bill. But I recently wondered what the result would be if I just did the minimum withdrawal each year, let the funds grow tax free and paid the very high tax bill upon the passing of the last surviving spouse.

Can a LIRA be transferred to an RRSP with no contribution room in Ontario?

Moving money from a LIRA or LIF to an RRSP or RRIF can have benefits. Here’s what to consider before you hit that transfer button, including tax implications.

Q: Can 50% of my LIRA be transferred to my RRSP if I do not have contribution room in Ontario Canada? Is it better to transfer to an RRSP or RRIF if funds are not needed and are used for investment purposes?

Bear markets: What’s a long-term investor supposed to do right now?

As we continue our way out of the pandemic, with inflation and dramatic market fluctuations, what is a long-term investor to do in a bear market?

Q: My mutual funds are doing terribly, and I know they always say that it is better to stay the course and ride out this market crash and whatever. But I’ve been thinking about divorcing my big bank for awhile now. I have RRSP with mutual funds that have high management fees with RBC, slightly better ones in Tangerine, as well as robo-advisor RRSPs in WealthSimple. If my RRSPs are tanking in RBC now anyway, is this a good time or a terrible time to divorce them and move all of my money to a robo-advisor ETF or something somewhere else?

I had a heart attack 5 years ago and recently retired. What are some tips for a good drawdown strategy?

Taxes will be Marko’s biggest expense in retirement.

Q: I am 67 and my wife is 62. I’m newly retired and haven’t started Canada Pension Plan (CPP) or Old Age Security (OAS) benefits. My assets include a holding company with $200,000, registered retirement savings plans (RRSPs) of $410,000, a tax-free savings account (TFSA) with $75,000 and $180,000 in a non-registered investment account. I had a heart attack five years ago. When should I start my CPP and OAS? And which accounts should I generally draw from?

What are the best investment options for cash in my portfolio now that bond returns are lagging?

Bond funds are posting negative returns, and returns over the past few years have been low. What’s the alternative?

Q: What are the best options for cash in an investment portfolio now that bonds are not working?

How do I get good financial advice so I don’t waste my money?

Stay curious throughout the planning process and you will get your money’s worth.

Q: I paid a fee-based planner for some financial advice, but they didn’t tell me anything I didn’t already know. I feel like it was a waste of money. Am I missing something?

What’s the real value of a robo-advisor?

With inflation, war and COVID, what are your options if you’re wanting a bit more from a robo-advisor? Do you have to watch your investments yourself?

Q: A few years ago, we transferred our investments from an advisor to a robo-advisor. When I checked our investments and saw that they had my husband, who’s in his 70s, invested upwards of 80% in equities, I was shocked and felt that was not appropriate for us. I suspect it was because they are able to move around and take advantage of opportunities they believe are worth the risk. I didn’t feel comfortable with that.

Am I paying too much in portfolio management fees?

Margarite pays $30,000 in fees for the management of her $2.5-million portfolio. Is that too much? If so, how can she lower those fees?

Q: My husband Jim and I have a $2.5-million portfolio of investments made up of stocks, mutual funds and exchange-traded funds (ETFs) with the wealth management branch of one of the Big 5 banks. Our annual fees, based on the size of our portfolio, were $30,000 last year. This seems exorbitant, given that about one-third of our portfolio is sitting in dividend-paying stocks that we don’t plan to sell.

Does it ever make sense to take CPP at age 65?

The math tells you to delay your CPP until age 70, but who lives their life based on the answer to a math question?

Q: I’m 62 years old and planned to take my Canada Pension Plan (CPP) at age 65. With all the talk about the benefits of delaying until 70, I wonder if taking it at age 65 is still a good decision?

Can I withdraw from RRSPs to pay bills?

Taking money from your RRSPs early to pay for debt has implications, including taxes, the loss of growth in the account, and more.

Q: What are the cons to withdrawing RRSP savings of $25,000 to pay off some unexpected bills I have incurred?

What’s the most tax efficient way to draw down my $5-million investment portfolio?

If we’re entering a prolonged inflationary period, you may be best to preserve and grow your capital as much as you can.

Q: I am 65 years old and my wife and I have pensions that total $95,000 per year plus a non-registered portfolio of $5 million that annually generates $95,000 in dividends. There is $2.3 million in unrealized capital gains in this non-registered account. We also have $2.5 million in registered retirement savings plans (RRSPs) and $240,000 in tax-free savings accounts (TFSAs). I am concerned the capital gains inclusion rate is going to go up from 50 per cent to 75 per cent, so I am thinking of crystalizing the capital gains on half of my investments this year by selling some equities. What do you think? I’d also like your opinion on the best drawdown strategy. Our current pension plus dividend income is enough for us, and we occasionally gift some money to our three kids.

Should I take CPP at age 60, even though I only have a small pension and no other investments?

Ryan is 59 years old and still has a mortgage. Should he apply for CPP now and use that money to pay down his mortgage, or invest?

Q: Hi, I’m 59 years old and fully employed. My annual salary is $70,000. I don’t have a registered retirement savings plan (RRSP) or other investments, but I do have a small pension from my employer that will pay me about $1,500 a month at age 65. I still have a mortgage of $200,000 at 2.4 per cent, as well as annual bill payments totalling $22,000. Should I apply for the Canada Pension Plan (CPP) now and use those funds to invest or pay down my debt? Or should I wait until I’m 65?

Do I really need 70% of my working income to retire comfortably?

There are various rules of thumb to determine if you have enough for a full retirement, but here’s a better way to determine it for yourself.

Q: I have read that in retirement you need about 70 per cent of your working income and I am just wondering if that is accurate? How do I know if I have enough?

Are fees for your TFSA tax deductible?

From HST to advisory fees, are the charges for a TFSA tax deductible? What is the savviest way to pay these costs?

Q: Can you also claim HST along with the advisory fees related to taxable investments that are non-registered investment accounts? I just want to be certain I can claim the HST that is paid with fee-based investments?

Should I follow my broker’s advice and invest in flow-through shares?

Scott’s RRSP contributions have been topped up, but he wonders whether flow-shares are a viable tax-saving investment for him.

Q: I made about $300,000 last year and expect to earn more this year. I maximize my contributions to my registered retirement savings plan (RRSP) every year, but I’m still paying a lot of tax. My broker says I should invest in flow-through shares, but they seem risky to me. Do you think I should invest in flow-through shares?

Can I retire at age 43 on $48,000 annually?

This will be tight, but you can do it, experts say.

Q: I am 43 years old and want to retire now on $48,000 net annually. I’ve worked 19 years and earn $95,000 a year. My investments include three rental properties worth $1.4 million with net income totaling $38,000 annually. I have a $700,000 principal residence, a registered retirement savings plan (RRSP) worth $90,000, a defined-contribution (DC) pension worth $60,000 and $20,000 in savings. All the properties have mortgages. Would I have to sell any properties to reach my goal? And should I pay off some mortgage debt before retiring?

Should I invest in a TFSA or RRSP? And when does it make sense to do both?

Whether you make less than $45,000 annually, or more than $220,000, there are some key points to keep in mind when deciding where to put your money.

Q: This is the time of year when I always look at the money in my savings account and try to determine if I have enough to make a registered retirement savings plan (RRSP) or a tax-free savings account (TFSA) contribution. With two kids and a mortgage, money is often tight and I can only do one or the other. How do I go about deciding which is best for me? And if I ever have enough money to do both — something that will likely happen shortly after my mortgage is paid off — does it make sense to do so?

How does a spousal RRSP withdrawal work?

Who can claim an RRSP withdrawal as income—the contributor or the spouse—and when it’s best to take any money out of the registered account.

Q: I bought a spousal RRSP in December 2019 and I plan to withdraw from it this week. Is it considered to be my income or my spousal income? I called CRA four times, but no one could answer this question for me.

Converting mutual funds: The benefits, the risks and the costs

How to deal with DSC fees when redeeming mutual funds and find out if it’s worth paying the fees. Sometimes it’s about luck.

My wife and I have been educating ourselves on the merits of ETF vs traditional mutual funds after deciding to make a switch from our personal financial advisor. We were late starters in saving and we have another 15- to 20-year investment horizon ahead of us before retirement stares at us.

Should we refinance our mortgage?

Rates are significantly lower than the one Jill and Bob have locked into until 2024. Would they save money by breaking their current mortgage?

We’re thinking about breaking our existing home mortgage to take advantage of low interest rates and would appreciate some guidance.

The tax implications of gifting adult children money and more

A reader asks about investing in his RRSPs after 71, withdrawing from RRIF and a sizable gift of money to his daughter would affect her tax-wise.

I am a widower, turning 71 before the end of the year. I have annual gross income of about $50,000, cash savings of about $500,000 left from the sale of my principal residence and an RRSP of about $1.5 million returning about 8%. I haven’t put anything into my RRSP for about 15 years. I also have a fully paid vacation property valued at $300,000. I am concerned that I will have to collapse some of my very productive investments to cover the government withdrawal rate of 5.28%.

How target-date funds can help you hit the retirement bullseye

Target-date funds are a simple investment option that make it easy for you to save and invest. But should everyone own one? Here are the pros and cons.

You’ve likely heard of target-date funds (TDFs) and wondered what they are and whether they should be part of your portfolio.

How do I shelter investment income through a corporation?

Accountants, lawyers and financial planners will all give you different advice when you’re deciding whether to incorporate. Here’s a road map to decide whether incorporation is worth it for you.

Q: How can incorporating help me shelter investment income? And at what point do I know if incorporating is worth it for me?

How to use life insurance to save tax and build wealth

Life insurance can be a lifelong financial friend whether it’s for estate planning, investing or as tax-free deposits into your account at retirement.

Financial planning questions often revolve around investing and retirement planning, but it’s not often someone takes a keen interest in integrating life insurance into their financial plan unless they have come across a particular strategy.

What’s the best long-term strategy for investing in a pension plan versus a TFSA?

Gina invests her TFSA money in a 50/50 split between equities and income. Should she invest the money in her defined-contribution pension plan differently?

Q : I have started a new job and my employer offers a defined-contribution (DC) pension plan that matches my contributions at five per cent of my annual salary. How should I invest this money? I was given a list of eight mutual funds to choose from. I’m 25 years old and invest my tax-free savings account (TFSA) money at a 50/50 equity-to-fixed income split and plan to continue with this for all my money outside the DC plan. But should I invest the money in the DC plan differently since I’m looking at a 30-year horizon? Also, what are the fees/MERs on these types of accounts? Should I consider opting out, and why?

Should I take CPP when I retire at 60 or wait until I’m 65 or older?

Delaying CPP makes sense in cases where you are able to collect the GIS and still maintain your lifestyle.

Q : I am 58 years old, a renter and would like to retire at age 60. I have a solid registered retirement savings plan (RRSP) invested in exchange-traded funds (ETFs) worth $300,000 (invested 70/30 in an equities/fixed-income mix), as well as investments in a non-registered account totalling $300,000 invested in the same way. I will need $50,000 net annually in retirement and am paying $1,800 a month for a two-bedroom apartment in a suburb of Toronto. Does it make sense to take my Canada Pension Plan (CPP) benefits at age 60 and defer withdrawals from my RRSP until a later date? Or, should I start making withdrawals from my RRSPs in two years and wait until I am 65 or older to draw my CPP?

How to get a grip on your cash flow to achieve your goals sooner

If you want to increase the amount of money you have to invest every month, here’s a road map to doing it right.

Cash flow is key to making your lifestyle goals possible and achieving financial freedom. If you get it right, you have money to invest, borrowing becomes easier, you can get the proper amount and type of insurance, and it puts you in control.

Is it time to search for bond alternatives for your balanced portfolio?

Understanding why you own bonds in the first place can help you decide on possible bond alternatives.

I was recently warned by someone in the financial sector that it’s not a great time to invest in bond ETFs. My current asset allocation is 60% equities and 40% bonds, so I’m wondering what alternatives would you suggest for that 40% portion of my balanced portfolio?

The pros and cons of using retirement planning software to help you figure out your needs

Test drive: The Canadians’ Preparation for Retirement — or CPR software — may be worth checking out.

Good financial planning software can be vital if you want to put yourself in a position to make smart, confident decisions while adapting to change, and learning the truth about your money — that is, what it will do for you.

Do you ever have a legal obligation to pay RESP money back to your parents?

Barbara wonders what a time-out from her studies might mean for her Registered Education Savings Plan, and if the withdrawals are truly hers to keep.

Q. I’m planning to take a break from university until I can move into my own place and support myself through school. I’ve already taken three years of classes, which I paid for through a mixture of loans, grants, and my Registered Education Savings Plan—which my parents set up and contributed to while I was growing up. I know it’s legal for them to dictate what I take from the RESP, but is there any situation in which I would be legally required to pay that money back to them?

The right time to start drawing from your RRSP/RRIF and non-registered investments

It often helps to think in terms of family wealth and tax efficiency.

One of the most asked questions the newly retired or those about to retire have is: “When should I start drawing from my registered retirement income fund (RRIF) or registered retirement savings plan (RRSP)?”

The Smith Manoeuvre strategy and how to use it — the right way — to your advantage

It’s a notoriously complicated investment strategy that uses debt to finance investments. Here’s what to know.

If you’ve heard about the Smith Manoeuvre, then you know it’s a smart, but controversial and often misunderstood financial strategy.

How to master your own financial plan for your own personal lifestyle

Most of us have no idea how much money we will need to live comfortably for the rest of our lives. Follow these steps to write a successful financial plan.

DIY investors probably have no trouble researching their next investment picks and making trades, but putting together their own financial plan takes things to another level since the resources for proper financial planning are not as freely available as they are for investing.

How does Purpose Investments’ new Longevity investment fund work and is it right for you?

The Longevity fund is unique, and so are you. It’s also getting a lot of media coverage and its launch is a good excuse to review your retirement income strategy. We run the numbers.

Many financial planners run financial plans based on the expectation of returning four or five per cent, but Purpose Investments’ new Longevity fund is designed to pay a 65-year-old a lifetime income of 6.15 per cent, based on the total amount invested with some inflation protection.

My three kids chose different educational paths. How do I withdraw RESP funds in a way that’s fair to them and avoids unnecessary taxes?

Q.I have a Registered Education Savings Plan (RESP) for my three children, the youngest of whom is starting university this fall. We have made some withdrawals for the older two kids but the plan is still well-funded. Our middle child has decided to pursue a co-op university program, which is essentially self-funded. When we contributed funds to the plan, part of the funds were put aside under his name and the government added grants to that. To be fair to him (and to avoid taxes), I assume there is a minimum amount that I should withdraw as an educational assistance payment (EAP) for him. What are my next steps?

How do I unscramble the alphabet soup of mutual fund classes?

Whether it’s A, D, F, I, or something else, almost every letter in the alphabet has been used to identify different fund classes.

Q:I’ve been investing on my own for about a year now. But I’m still confused about the different types of mutual fund share classes. What do they all mean? And how do I go about choosing the right one for investments ?

What place should cannabis and cryptocurrency ETFs have in my portfolio?

What’s right for you all comes back to the basics of accumulating wealth and building a portfolio.

How compound interest can turn one penny into over $5 million in 30 days?

It’s been called the most powerful force in the universe. Here’s how to learn to love compound interest and let it make you rich.

What are ‘alternative investments’ and are they for me?

Alts are different, and those differences will lead you to wanting them or not in your portfolio, along with your risk tolerance and investment goals.

Everything you need to know about investing in split shares

Both conservative and aggressive investors can take advantage of leverage by doing the splits.

Not many investors are familiar with split shares and while they appear complex, they provide opportunities for both conservative and aggressive investors.

They were created with a dash of creative financial engineering by taking a pool of dividend-paying stocks, and splitting out the dividends and growth into two different exchange vehicles: a preferred share and a Class A share.

Can I retire at age 63? And when should I convert my RRSP to a RRIF?

If Paolo withdraws cash too early, he could run out of money.

Why every investor should be in love with dividends

Want to retire early, pay less investment tax and earn ‘free money’ along the way? Here is absolutely everything you need to know about dividends.

Are single seniors unfairly penalized at tax time?

Karen wonders if her latest tax bill is too high, and whether there’s a way to avoid the social benefits repayment.

Q. I am a senior with an income of about $115,000, single and in receipt of $7,364 in OAS benefits annually. I keep only about $200 a year out of that for myself. Yesterday, while doing my income tax return, it worked out that I ended up owing an extra $2,000 to $3,000 in income tax, although nothing else had changed in my money situation. Is this due to the social benefits repayment and, if so, can I have OAS payments stopped? Or am I going to have to pay the social benefits recovery no matter what I do?

Reality-testing your financial plan

John’s advisor seems impressive, but he’s left out an important consideration: What kind of lifestyle does his client want in retirement?

Q. I am contemplating changing financial planners and I just met with one who seemed very impressive. Within about three hours he had everything laid out for me: the investments I should purchase, the use of life insurance, delaying CPP to 70 and more. Still, I would like to get a second opinion before I make my move.

Is probate an inevitable cost for a surviving spouse?

Sandra and her husband have lived in their principal residence for 40 years, but his is the only name on title. A financial planner looks at their options.

Q. My husband and I have lived in our principal residence for 40 years. The house is held solely in his name, and I am the beneficiary of his will. Would the house have to be included in probate of his estate, should he predecease me?

Why do I need a financial plan?

A financial plan helps you consider—and revisit as needed—important questions about how you want to live. What is important to you? Are you going to have enough or too much money to do those things? Are you taking unnecessary risks to maintain your lifestyle?

Q.I am in my early 50s, have a steady job, I’m not a big spender, and I make RRSP contributions. Why would I need a financial plan? I don’t see how it could help me.

How do I become a money coach in Canada?

Although regulatory requirements in most provinces permit you to provide financial advice or coaching with no education or experience, you’ll need appropriate licensing if you want to provide your clients with financial products such as insurance, mortgages and investments.

Q. I was reading an interesting MoneySense article entitled, “Should you change careers and become an investment advisor?” and I was wondering where someone can get their qualifications or certifications to become a money coach in Canada. I’ve tried some general web searches but it hasn’t turned up much.

Should we refinance our mortgage?

Rates are significantly lower than Jill and Bob have locked into until 2023. Would they save money by breaking their current mortgage?

Q. We’re thinking about breaking our existing home mortgage to take advantage of the low interest rates we’re seeing now, and would appreciate some guidance. This is our scenario:

Mortgage principal: $572,000

Weekly payments: $746.00

Interest rate: 3.78% fixed and locked in until December 2023

Penalty fee for breaking mortgage: $33,000

Unconventional ways of investing in a family RESP

Surprise: a lump-sum contribution is likely to result in more money, even though you forgo government grants. Plus, reassurance for blended families who want to hold a family RESP with both parents as joint subscribers.

Q. We have had a family RESP for many years with three beneficiaries: a son of mine from a previous marriage and two kids of our own. I have been the only subscriber for the RESP as it is my understanding that in order for there to be joint subscribers (that is, myself and my wife), all beneficiaries must have a blood relationship with all subscribers. That rules out my wife as a joint subscriber, as she obviously does not have a blood relationship with my son from my prior marriage.

The upside to waiting until age 70 to take CPP benefits

Consider your life expectancy and probable return when making your decision about whether to take government pension benefits as soon as you retire, or to wait.

Q. I am retiring next year at age 65 and I don’t know if I should take my CPP immediately, or wait. My friends and other people I know from work took their CPP when they retired and they are telling me I should take it when I retire. Are they right? When is the best time to draw CPP?

Timing the withdrawal of RRSP savings to minimize your tax hit

Ellen has been holding off on drawing from her retirement savings in the hope that she can avoid clawbacks to her government benefits. Understanding how benefits are calculated is the first step toward figuring out her options.

Q. I’ve been fully retired since 2018, and living only on government pension (QPP, OAS and GIS). I have some RRSP and TFSA investments, and would like some help with determining when I should start withdrawing funds—and whether I will need to pay tax. I’ll be turning 71 in December 2021.

Winding down self-employment and planning for retirement

At 60, Deborah is looking to work less and spend more time by the water, where she’s happiest. But can she reduce her debt without selling her home?

Q. I am a 60-year-old female, working full-time employed/self employed on a 100% commission basis and averaging between $107,000 and $140,000 gross annual income.

Should Kathy take monthly payments or the commuted value of her pension?

A lump sum could allow for some investment opportunities, but that option requires self-control to avoid overspending early in retirement.

Q. I am torn about making a key financial decision in my life. First, a little about myself. I worked for about seven years (actually, six years and 360 days) as a teacher in the Arctic. I resigned this year and have returned to the “south.”

What to consider before transferring RRSP money to a company pension plan

Looking at historical returns, Jaspal figures he could earn significantly more by pooling his individual retirement savings with his employer’s plan—but there’s more to consider.

Q. A few years ago, I joined a public sector employer with a hybrid defined-benefit, minimum-guarantee pension plan that will allow me to move RRSP contributions made elsewhere, into the employer’s plan.

Is it best to own a first home as an income property or primary residence?

Larry wonders if he will lose his ability to use first-time home buyers’ programs if he rents out the townhouse he’s purchased before he lives in it.

Q. I would like to know whether it is better, financially speaking, to own my first house as an income property, or as my primary residence in Ontario. I am single, living with my parents, earn a steady income and have $80,000 in savings. I’ve already purchased a new-construction freehold townhouse for $320,000 (paid $30,000 in deposit), which will close in August 2020. While I had been planning to rent out this property, I’m wondering if it is better to treat it as my primary residence initially, to take advantage of all the benefits available to first-time home buyers (including the ability to borrow from my RRSP), then change to a rental later.

Is this couple on track to leave their 3 kids an inheritance?

Bob and Janet are DIY investors seeking advice on how to reach their estate-planning goals. They can improve their already good financial situation by implementing some tax-saving and wealth-building strategies.

Q. My wife and I are wondering whether we are on track to leave each of our three children an inheritance of $250,000. I’m 63 years old, retired and receiving a monthly OPTrust pension (a type of defined benefit pension) of $3,400 net. When I turn 65, this pension amount will be reduced to about $2,700 net monthly as it is integrated with my CPP.

How to protect family RESPs from being raided

Morley is concerned about the education savings he’s putting aside for his son’s twin boys. What happens if their mother withdraws the RESP money “for her own purposes?”

Q. I am a grandparent providing funds for a family RESP. It is for twin grandsons—my son is the father. I have a bit of a concern their mother may decide to withdraw the funds I provided for her own purposes. Is there a mechanism whereby both parents have to sign off if the contributed funds were to be withdrawn and not used for the children’s education?

What to do with a rental property when you owe more than it’s worth

Oil prices have tanked and Renee wants to sell her rental property in Fort McMurray, but she owes more on the mortgage than the property would currently be listed for on the market. What should she do?

Q. I bought a home in Fort McMurray, Alta., for $413,000 in 2007. Five years later, in 2012, I moved out and started renting the property, and it has remained an income property since then.

Using life insurance to leave your kids an inheritance

Like a reverse mortgage, you would borrow against the policy’s cash value. When you pass away, the loan is paid off with the tax-free life insurance death benefit and the remaining insurance is paid out to your children tax-free. Here’s how it can work.

Q. My wife and I are both 57 years old. I have a business in Ontario, from which I earn $260,000 a year, and my wife makes $40,000 at her job. We have maxed out our RRSP contributions and we will soon do the same with our TFSAs.

Retirement strategies to keep more money in your pocket

From income withdrawal strategies to the right software for DIY retirement plans, Peter wants to know the best ways to maximize his retirement nest egg.

Q. I retired seven years ago, when I was 55. I’d like to run projections and analyze the best way to draw down my RRSPs with the least amount of taxes payable. Is there a software package you’d recommend that can do this?

How to get a bigger benefit from your RRSP contribution

Invest with before-tax dollars if you can, and don’t let the resulting tax refund get swallowed by by day-to-day expenses.

Q. I am a hairdresser and my retired clients are telling me not to contribute to RRSPs because of all the tax they have to pay on withdrawals. Instead, they say I should contribute to a TFSA because the withdrawals are tax-free. What should I be doing?

Is Carol better off withdrawing all the money from her RRIF now?

At age 73, she believes this strategy will allow her to claim additional Guaranteed Income Supplement and and rent subsidy benefits.

Q. I am considering deregistering my Registered Retirement Income Fund (RRIF) of $89,000 and taking the tax hit for the 2019 tax year. Doing this would leave me eligible to maximize the Guaranteed Income Supplement (GIS) as well as the Shelter Aid for Elderly Renters (SAFER) in the future.

What’s the best way to help a relative, financially?

At 30, David’s nephew is living on close to minimum wage, with no retirement savings. An RRSP isn’t the best choice, because withdrawals will count as taxable income that may reduce government benefits. But there are other options.

Q. My nephew is 30 years old and works full-time in a close-to-minimum-wage job. He carries a mortgage on his condo and is able to save about $40 per paycheque. Periodically, he contributes to his TFSA but still struggles financially. I fear that he will not have saved sufficiently to fund a comfortable retirement.

How much should you give to charity?

You’ll want to consider how much you want to give, as well as how much you can afford, and when to apply the federal and provincial tax credits your donations qualify for.

Q. Can you share any thoughts on what is an appropriate amount to give to charities annually? I have often heard it expressed in terms of a percentage of household income. Also, are there any tax credits for charitable giving that, as a middle-income Canadian family with household income of $150,000 annually (evenly split between me and my spouse), we should be aware of for the 2019 tax year? And how could I make full use of those credits?

Is Dane, 50, on the right track with his early retirement strategy?

To bridge the gap between his last day of work, and the start of his defined-benefit pension payments at age 60, he plans to draw funds from laddered GICs.

Q. I’m 50 years old and I’d like to work for three more years, then “retire” at age 53. I’m single and have two defined benefit pensions that I could begin collecting at age 55 but want leave them untouched until I turn 60 as that allows me to qualify for full pensions.

Ready, set…retire?

At 49, Simon has about $600,000 in registered and non-registered investments, and wonders if it’s enough to live on through his golden years.

Q. I need some help figuring out what to do with my nest egg. I have always done my own investing and returns have been pretty good. However, this year at age 49, I am unexpectedly retired and would like to stay that way. I had liquidated most of my assets to start fresh with a “cash-flow” income-generating, retirement-type portfolio but I am kind of stuck on how to go about it building one.

Should James take a lump-sum pension buyout and invest the money himself?

Upon closer consideration, many people find that keeping their guaranteed pension payments leaves them better off.

Q. I work for the provincial government of one of the Atlantic provinces. I will be 55 next year and will have 29 years of service; I’m ready to retire.

When your investment partners don’t play by the CRA’s rules

Marcus and some friends turned a profit on their investment property. Trouble is, two of them plan to keep the income a secret from the Canada Revenue Agency. How can Marcus protect himself?

Q. Three friends and I pooled our money ($100,000 total) two years ago as a down payment to buy a rental condo in Toronto. All four of our names are on title. We flipped the condo this past May for a total profit of $120,000 after expenses. That’s a $30,000 capital gain for each of us, which is pretty good.

How to leave money to an adult child with no investing know-how

Dee wants to ensure that her son receives a regular monthly income, while protecting the lump sum of his inheritance. What are the options?

Q. When my husband and I pass away, our only son will be in line for a significant inheritance. Being realistic about his capabilities, we need to pass along this legacy in a responsible way; our son will not be capable of handling a lump sum. Our wish is to have the money reach him in monthly increments throughout his entire life, and also to protect it from a future spouse should that marriage fail. We have no other close relatives and are considering putting the money into a trust, but my understanding is that the funds would be taxed at up to 53%. Are there any alternatives?

How safe is it to keep more than $100,000 in one savings account?

Marcus and Rina have socked away $120,000 for a down payment in a single savings account at a small credit union. Should they be worried?

Q. My wife, Rina, and I are in our late 20s and are saving up for a downpayment for a home. We have $120,000 in our account and are trying to reach $200,000 so we can make at minimum a 20% downpayment on a $1 million detached home in Toronto. My question is, how safe is our money in one account? Are small institutions like my credit union a risky place to keep over $100,000 in savings? And should we consider different account options for the savings?

Tax-reduction strategies don’t need to be complicated to work

Lou, 39, is curious about flow-through shares and other tax-enhanced investment options.

Q. I’ve done some research into tax-enhanced investment options, including corporate-class or swap-based funds, investments that pay a return of tax-free capital, flow-through shares, and life insurance strategies to help reduce taxes. When should someone consider these investment options and how do they determine which one is best for them?

What’s your investing “why?”

Instead of focusing on target returns, start with what you want the money to do for you and your family.

Q. My wife and I are in our 40s and about to receive a sizeable (for us) inheritance. We want to generate a minimum 8% annual return on the money and keep it safe, while at the same time minimizing taxes. We’re looking at putting the maximum allowed into the TFSAs of six family members, totalling roughly $350,000 since we think it’s a good way to minimize taxes. Is there anything else that we should be considering in this fortunate situation?

Beyond financial planning: How to achieve the lifestyle you want

Newly mortgage-free, Mara is looking to invest $26,000 annually. But does that mean putting off life goals she could be enjoying today?

Q. I have just turned 40, am single, and earn $86,000 a year. I also have zero debt. I just finished paying off my house, worth $315,000, and I would like to continue to put away my mortgage payment of $1,000 every two weeks as savings.

Using a HELOC as an investment strategy: not as taboo as you might think

Should Martha leverage the equity in her home to invest in dividend-paying investments—and what are the tax repercussions?

Q. I wish to leverage my home equity line of credit (HELOC) to invest in dividend-paying investments. How would you advise I approach this? Is this an effective tax savings tool? Is there any financial institution or products you would advise?

When does investing in flow-through shares make sense?

And is the possibility of capital losses down the road worth the added risk?

Q. My wife and I are nearing the end of our working careers. We are big planners and have a financial plan that we have been successfully working with for over 15 years. My wife will be retiring from teaching in two to three years with a full pension. As a part of our plan I left my job this May prior to my 50th birthday to pull my Pension (I know this is a controversial move, but did I mention our 15-year plan?), I am planning on returning to work for the next few years.

She’s 34 and wants to retire at 65 with $70,000 a year. Can she?

Jenna’s quick calculations show she’ll need $2 million in savings. Is that really true?

Q. I need some advice on saving for retirement. I’m 34 years old and hope to retire at age 65 with a gross annual income of $70,000. I currently earn $110,000 a year from my job at a law firm.

What’s better, a LIRA or an enhanced pension?

And which is best if Craig wants to leave money to his kids?

Q. I plan on retiring in the next year. I will have BC Municipal Pension Plan income as well as about $400,000 dollars in my Special Agreements (SA) account. Just to clarify, an SA is a unique feature of BC pensions. The contributions can be transferred to a locked-in retirement vehicle or used to increase your lifetime monthly pension—you choose. I have been employed with the same company for 32 years. So when I retire, I have to make one of these two choices with my SA—leave the money in the pension and receive it added on to my monthly pension OR put the entire amount into a locked-in registered retirement fund (LIRA). I am not sure what the benefits of each would be, and which I should do. I do like the idea of putting it into a locked-in fund, separate from my monthly pension income so that whatever is remaining when I die, will go to my children. Any advice you could give would be much appreciated.

Should I invest my money or buy a life insurance policy instead?

Which makes more sense if Alessandro wants to leave money to his kids.

Q: My wife and I are both 40 and have two kids—ages 5 and 7. We are considering buying a joint last-to-die life insurance policy that would cost a fixed $7,105 per year for ten years. That’s a total of $71,050 and the policy would pay $500,000 when the last of us dies. This is a proposition from our advisor after we have made our retirement plan. We have concluded that we have enough savings to retire at 55 with a very comfortable nest egg made up of TFSAs, RRSPs, and defined benefit pension plans, as well as money in non-registered investments.

At 66, borrowing to invest in a TFSA isn’t a good idea

Dawn has never had a financial plan. She should pay off her debt and focus on maximizing government tax credits and benefits.

Q. I am 66 years old and have not had a good financial plan, but hope to work for another 5-10 years. I own my condo and will have it paid off in full in 5 to 6 years. I also have no savings to speak of—except for $12,000.

Are annuities, bonds or GICs best for an 80-year-old’s money?

Terry has done well with higher yield shares and ETFs, but is worried about rising interest rates.

Q: My wife and I receive about $2,500 a month each in pensions. Plus, we each have about $75,000 in our TFSA accounts and about $180,000 in our RIF accounts. I have never been a fan of bonds, so for the last few years, I have invested in higher yield shares and ETFs. This has proved very successful and has supplemented our pensions generously so that we can travel four or more times a year.

How should a new Canadian invest his extra cash?

Should Adam add it to his TFSA? Or pay down the mortgage on his properties?

Q. I am a new Canadian (27 years old) and started working in Canada about 1.5 years ago. It took me a while to figure out how things work in this country and a few months ago, after ditching a financial advisor who was also a family friend, I started investing on my own.

How to invest for an unexpected early retirement

Should Danny downsize, invest differently, or clear his debts?

Q: I need some advice. I have a LIRA worth $21,000, an RRSP worth $92,000 and a TFSA worth $38,000. I’ve also been divorced for three years now and I live alone most of the time.

Can Anne, 63, afford to retire right now?

Or will she run out of money?

Anne, a 63-year-old divorced human resource manager earning $100,000 annually, retired a year ago and has been living off a small $45,000 inheritance. But she is worried. “I don’t have a company pension so I will have to start drawing down my investment portfolio later this year,” says Anne. “I am concerned that I won’t have enough money. I know I can return to work if I have to but I don’t really want to. And even though I have an advisor, it would be great to get a second opinion on whether my money will last for my lifetime.”

How should a 24-year-old invest a $500,000 inheritance?

Is investing it all in the stock market a good idea? Or should Eric consider a rental property?

Q: My parents recently passed away and I inherited close to $500,000. I am 24 years old working as an engineer-in-training in Toronto with an annual salary of $65,000. My student loans are paid off and I carry no credit card debt. I currently live off my own salary with about 40% of my after-tax income going towards rent and car payments. I put 8% of my salary towards a company matched RRSP and they match an additional 4%. My TFSA is capped in a mix of ETFs.

How to give your kids TFSA investment advice

Rosie is considering helping her kids choose an ETF for their TFSAs but isn’t sure which one is best.

Q: I would just like to get some tips on how to advise my young adults on where to invest their money. They are ages 22 and 23. It’s for their TFSA.

How to invest a $240,000 inheritance

Shirley is 65 years old, retired, and considers herself a conservative investor. What should she do?

Q:I am 63 years old, and stayed home to raise my family for a number of years, so do not have a lot of employment years or high income. I am currently working, but my health is slowly diminishing due to rheumatoid arthritis and not sure how much longer I can work full time.

TFSA penalties for holding foreign investments

What are “permitted” as well as “non-qualified” investments?

Q: I have a TFSA and have read a lot about investing within a TFSA, but one area is still a question mark in my mind— investing in equities or funds that are on an exchange from outside of Canada or equities that are listed on the TSX or Venture exchanges but have out-of-country holdings. So my question is:

Easy way to calculate capital gains tax on DRIP shares

When you have no records, it can be difficult. Here’s advice.

Q: I purchased 100 Bank of Nova Scotia dividend reinvestment plan (DRIP) common shares @ $30.60 in 1994 and have since added 300 shares through their Optional Cash Purchases at different intervals. My account today has a balance of almost 950 shares in total @ $77.00 (certificate shares and drip shares).

What’s the safest, most tax-efficient way for Jim to invest $500,000?

Try paying down debt.

Q: I have $500,000 coming to me soon from a property sale and am looking for the best fixed-income product to invest in. I have no immediate use for these funds but I’m hoping it can be tax efficient too. Any suggestions?

Best investment strategies for newcomers to Canada

This family has an extra $10,000 they’d like to grow.

Q: I will be immigrating to Canada in November with my spouse and three children, and I need advice on the investment opportunities a new immigrant can take advantage of. We have done a budget of our landing costs and have realized that we have an excess of $10,000 CAD outside the cost of living expenses for six months.

How much to save and invest to cover inflation for 40 years

This woman’s $50,000 annual DB pension won’t be indexed.

Q: I’m pretty lucky to have a defined benefit pension from my employer. I will receive $60,000 annually from it in five years. Unfortunately, it will not be indexed. How can I calculate the amount of saving that I need before retirement to cover the inflation for 40 years? I want to keep the same power of buying.

What to do with a $2.4 million retirement portfolio

Paul also has $130K a year in pension income for life.

Q: My wife and I have a portfolio of about $1,600,000 in dividend-paying stocks that include banks and financials, REITs, pipelines, utilities, some ETFs tracking Canadian and U.S. high dividends stocks and the US S&P 500, and ETF tracking all the world except Canada. We also have $800,000 in GICs and high-interest savings accounts. We are also fortunate to have Defined Benefit pensions and annuities producing about $130,000 in income per year. My question is, what should I be doing with our investments at this point? We have more than enough to live on and won’t likely ever spend all this money. We are both 77 years old.

Should you sell mutual funds with DSC charges?

Katrina could lose thousands and wonders if there’s a better way.

Q: I had a Life Income Fund (LIF) with one of the Big Five banks and a few years ago I met a person who said he could make my money grow faster with his company’s mutual funds. I decided to invest with him. Two years on and I’m losing money on it, and not due to the stock market’s performance. So I’ve decided it’s best to move my money back to the Big Five Bank. I have been told now that I will have to pay a Deferred Sales Charge (DSC fee) in order to do so. I was never advised of this fee or told that there would be implications if I moved my money down the road, at the time that I signed my money over to them, and now I could lose thousands just to move my money. Is there a way to fight this? I’m not a savvy investor, and I think I’ve been had!

Best way to allocate cash in a $1.4 million retirement portfolio

This 66-year-old retired couple’s portfolio is more than 25% in cash. Where should they put it?

Q: My wife and I are both 66 years old, retired in British Columbia, and have no kids (that I know of!) We both receive CPP (about $550/monthly each) and full OAS ($470/monthly each). About 10 years ago, we both agreed to get rid of our financial advisor and manage our portfolio ourselves. Out of interest and because I enjoy investing as a hobby, I decided to manage everything myself, sharing information on our investments with my wife a few times a year (she has no interest in investing herself.)

Spousal RRSP or TFSA: The best option for a retired couple

If you want to prolong your retirement money, try the RRSP. But for estate planning, a TFSA may be the better choice.

Q: When my husband turned 60 we set up a spousal RRSP account for me and put his $800 monthly Canada pension cheque into it. We did this because I was a stay at home parent and there will be no pension for me. Now, five years later the balance is at $55,000. My husband is now retired, we live on his employer pension and continue to put his Canada pension in this spousal RRSP that was set up for me. I’m not sure this is the best way to invest that money. Should we be looking at other options? If so should we leave what’s already in the RRSP where it is and start doing something else with new contributions? Again, we contribute about $800 each month.

Can a TFSA be invested in a life annuity?

Brian has been told that he can’t. What are his options?

Q: I read on an insurance broker’s blog it’s possible to have an annuity within a TFSA so the payout would happen within the TFSA, and I’ve been trying to have that set up for months. I contacted eight insurance companies, and they all said it’s not possible. Instead, they suggest their lifetime income products such as Guaranteed Investment Funds (GIFs) so I’m confused. Can you have an annuity within a TFSA or not? And if so, how and where can it be done?

Is taking CPP at age 60 the best option for a lower income earner?

Lisa needs a good strategy.

Q: Is taking CPP at age 60 the best option for a lower-income working person? Is it really leaving money on the table to wait until age 65 to start taking it? I have a yearly income of about $47,000 now and a company defined contribution pension plan worth about $200,000 with my employer. What’s the bests strategy to maximize my income in retirement?

My advisor sold me high-fee funds. Should I dump her?

Remember, fees are only one part of your advisor relationship. And you can get them lowered.